The interest rate on Apple Card's savings account was today lowered from 3.65% to 3.50%.

Push notifications regarding the cut were sent to Apple Card users on Thursday. Savings account interest rates often fluctuate with changes made by the Federal Reserve, and when rates are lowered, banks cut their annual percentage yield (APY). That said, today's cut doesn't appear tied to a specific Federal Reserve move.

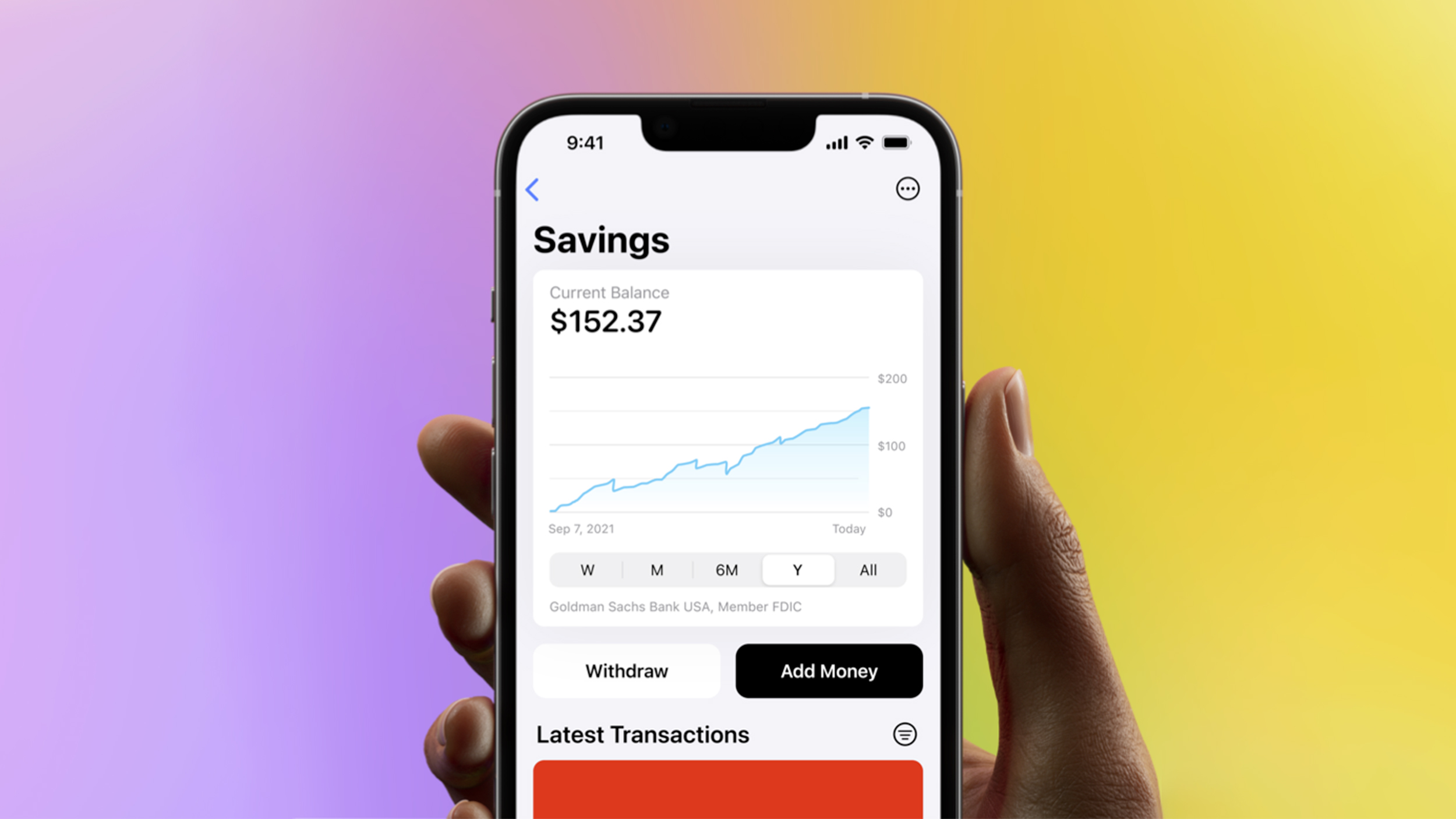

Apple introduced its savings account in April 2023, partnering with Goldman Sachs. Designed for Apple Card holders, the account is exclusively available to U.S. residents aged 18 and above. It can be managed through the iPhone's Wallet app, offering a user-friendly experience with no fees, minimum deposits, or balance requirements.

The account allows users to earn interest on their Daily Cash cashback balance, as well as on funds transferred from linked bank accounts or Apple Cash balances. Initially capped at $250,000, the maximum balance has since been increased to $1,000,000.

In January 2026, JPMorgan Chase reached a deal to take over operation of the Apple Card, with the transition expected to take approximately two years.

Alongside its new Apple Card partnership, JPMorgan Chase will reportedly launch a new Apple savings account, but existing users with Apple savings accounts at Goldman Sachs will not be automatically transitioned and will need to decide whether they want to stay at Goldman Sachs or open new accounts with Chase. Apple has a FAQ about the transition.

Article Link: Apple Lowers Savings Account Rate for Apple Card Users