Got a tip for us?

Let us know

Become a MacRumors Supporter for $50/year with no ads, ability to filter front page stories, and private forums.

Apple Preparing to Launch Apple Card Savings Account

- Thread starter MacRumors

- Start date

- Sort by reaction score

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

The large banks all seem to be around 4% or lowerGiven the current market condition, anything lower than 4.8% APY is a flop. (tons of 5%+ high yield saving offers out there)

You’d have to go to a regional or smaller experience for higher, which tends to mean worse apps and accessibility.

Do you recommend any?

It's UK, Royal Bank of Scotland.Where in the world is this? That barely keeps up with inflation but its way better than I am getting.

I use it all the time. I pay my rent in apple cash.BTW, do many people use Apple Cash? I don't see it mentioned anymore.

The real question is does anyone use Venmo anymore?

This hurts in so many levels 🤣🤣We've finally reached a point where we have minimum OS requirements to open a bank account... never thought I'd see the day.

I used Venmo today since Starbucks partnered with them recently as a payment method in their app.I use it all the time. I pay my rent in apple cash.

The real question is does anyone use Venmo anymore?

You say tons, I can't find 1. Please share 1 large bank offering that.Given the current market condition, anything lower than 4.8% APY is a flop. (tons of 5%+ high yield saving offers out there)

Wish they would do something like the Revolut card with Apple Pay, anywhere in the world just pay with your phone through an Apple account rather than having to change into different currencies and exorbitant credit card charges.

Nothing large (unless the original poster knows of one that I am not aware of) but there are a handful of small regional banks offering slightly over 5% and many others that are just under (but getting very close to) 5%.You say tons, I can't find 1. Please share 1 large bank offering that.

Super-regional BMO Harris has a savings account (in certain regions like Las Vegas) that offers 4.3%. That’s one of the highest for a big bank I’ve seen so far.

Where in the world is this? That barely keeps up with inflation but its way better than I am getting.

NatWest / RBS in the UK:

Digital Regular Saver | Regular Savings Account | NatWest

Get rewarded for regular saving. Save £1-£150 each month with a Digital Regular Saver account, our instant access monthly savings account. Apply online.

Goldman Sachs, whose primary business is investment banking and providing advice to the ultra-rich, has a retail bank, Goldman Sachs Bank USA, that it launched a few years ago to expand its client base to mainstream banking customers. The brand name on the bank’s offerings, as Apple Card users know, is Marcus. Goldman Sachs Bank USA, which is a wholly owned subsidiary of GS, is fully regulated (its main regulator is the Federal Reserve, which isn't the case for every bank) and insured (through the FDIC) by agencies of the federal government. These are the same agencies that oversee the systemically important banks in the US, including JPMorgan Chase, Citigroup, Bank of America, and Wells Fargo.

Marcus has been an Apple partner for a few years because it wanted to acquire customers quickly. Currently, though, Marcus has not been performing as planned. As a result, GS has said during recent earnings announcements that it has been ramping down the amount of attention Marcus gets relative to GS’s other activities.

The last time I looked, the 3.75% APY on savings is also available at other online-only banks, including American Express Savings Bank. So the rate is competitive at the moment…but could change at any time.

I believe the question is what bank was giving 6% in the screenshot that @Reason077 posted.

So if I have let's say $10,000 in my Apple Savings Account. How much interest will I earn after like 1 year? I'm wondering if it's worth it for me to transfer all my money over from bank of america savings or chase savings account to the new Apple Savings. I believe bank of america has only like a 0.03% APY which is extremely bad compared to Apple's 4.15%.

If no money moves in or out except interest it depends how often it compounds:So if I have let's say $10,000 in my Apple Savings Account. How much interest will I earn after like 1 year? I'm wondering if it's worth it for me to transfer all my money over from bank of america savings or chase savings account to the new Apple Savings. I believe bank of america has only like a 0.03% APY which is extremely bad compared to Apple's 4.15%.

Yearly would be $415. Monthly would be $422.99

I thought the more you have in your savings, the more interest you will earn? Does anyone know how often it compounds?If no money moves in or out except interest it depends how often it compounds:

Yearly would be $415. Monthly would be $422.99

You’re right, and with the Apple Savings account, interest is compounded daily and credited to the Savings account monthly.I thought the more you have in your savings, the more interest you will earn? Does anyone know how often it compounds?

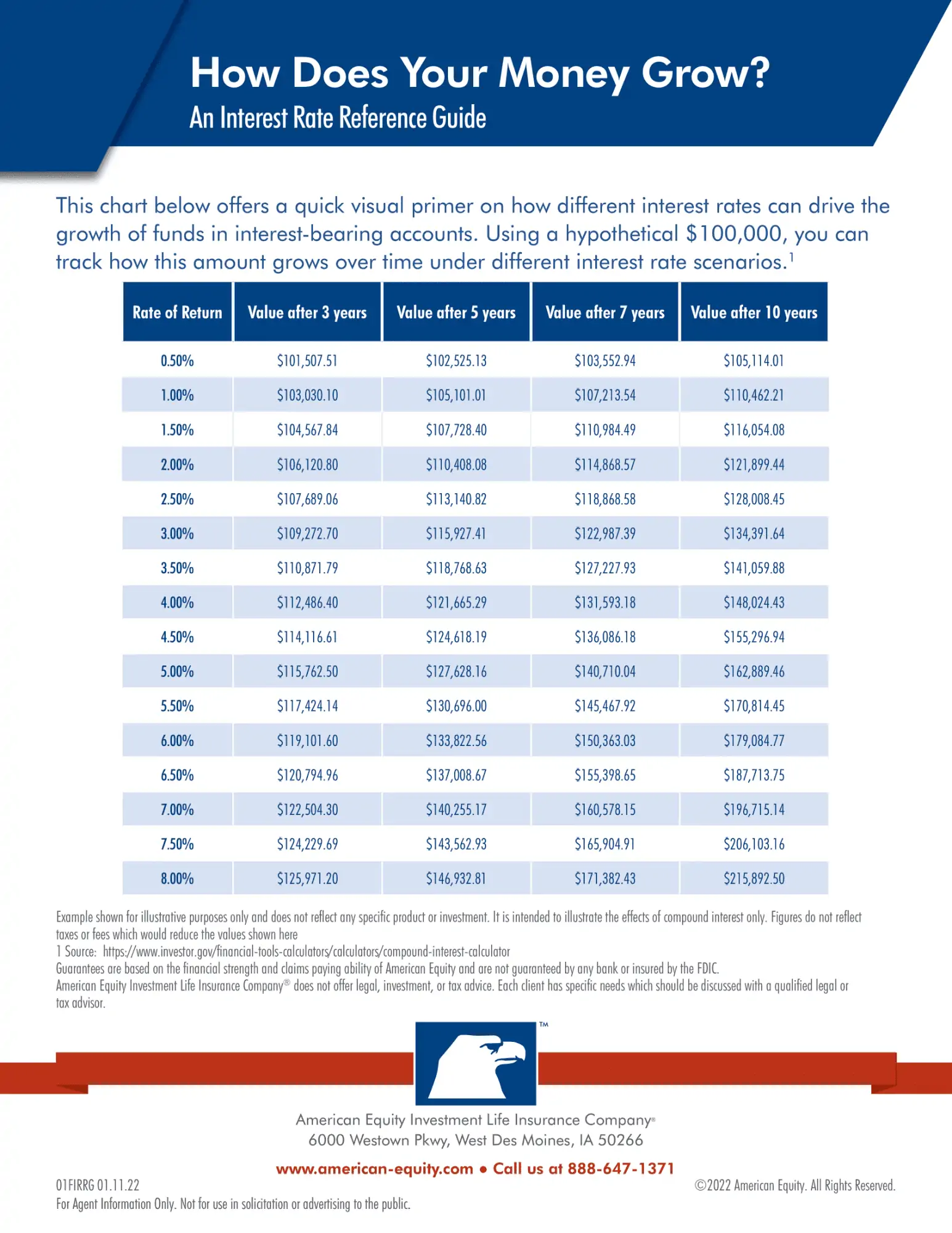

If I entered the information into the tool right:

Compound Interest Calculator

Utilize this free compound interest calculator to solve a rate of return on an investment on a daily, weekly, monthly, quarterly, and annual basis.

Update: I needed to zero out the “Additional Contributions” field to be correct, I think. So, more like $1,0424, or $424.00.

Last edited:

It took me seconds to sign up and redirect my Apple Card cash back. For now, that's all I'll use it for as my bank responded by bumping my savings account up to 4.20%. 😅

The interest rate likely won’t be 4.15% for the entire year and will decrease whenever the Fed decides to cut rate (this is expected to happen at some point later this year).So if I have let's say $10,000 in my Apple Savings Account. How much interest will I earn after like 1 year? I'm wondering if it's worth it for me to transfer all my money over from bank of america savings or chase savings account to the new Apple Savings. I believe bank of america has only like a 0.03% APY which is extremely bad compared to Apple's 4.15%.

Apple was smart to release this product at the peak of high rates to more effectively capture customer deposits. When rates decline, people likely won’t move their money, but new customers will be less incentivized to put their money there.

All other banks will probably lower their rates as well though, so same diff.The interest rate likely won’t be 4.15% for the entire year and will decrease whenever the Fed decides to cut rate (this is expected to happen at some point later this year).

Apple was smart to release this product at the peak of high rates to more effectively capture customer deposits. When rates decline, people likely won’t move their money, but new customers will be less incentivized to put their money there.

Which is why I said people likely won’t move their money. Just giving people a heads up to not expect a fixed 4.15% throughout the year.All other banks will probably lower their rates as well though, so same diff.

Won’t new customers have the same incentive as now? That being, when everyone’s rates drop, Apple’s will still be higher than most banks?new customers will be less incentivized to put their money there.

Just an FYI but I am trying to link an external bank checking acct. and I received the email notice that it has been linked but needs to be verified and to call Goldman Sachs. So far, on hold 54 minutes. HHHHHHHH

And the chat is so worthless too. I tried to ask something on break at work. Still hadn't answered by the time it was over. Then next break it has been closed. Why can't they just save it until I come back and answer again??? And they never fix anything anyhow. They still can't figure out why some merchants still want our old ZIP Code when we moved FIFTEEN months ago. And is it only some? Someone said they had a similar issue with money going to their Apple Savings. Random merchants the money will never show up.Just an FYI but I am trying to link an external bank checking acct. and I received the email notice that it has been linked but needs to be verified and to call Goldman Sachs. So far, on hold 54 minutes. HHHHHHHH

>4% is a pretty compelling rate. Tell someone it’s ~2%, they will be more indifferent to just keeping it in their checking account or would rather invest it in the stock market. As a whole, Apple and other higher yielding saving opportunities would see lower inflows from consumer in a lower rate environment (the pie gets smaller). However, you’d assume that Apple would still capture a larger share of those inflows if they’re paying the most competitive rate.Won’t new customers have the same incentive as now? That being, when everyone’s rates drop, Apple’s will still be higher than most banks?

3% is a compelling rate if someone has their savings in a bank that offers 0.04%, though. Which is what some other banks are offering currently. If Apple goes down to 3% those others could drop to 0.01%… and the 3% would STILL be a better investment than that.>4% is a pretty compelling rate. Tell someone it’s ~2%, they will be more indifferent to just keeping it in their checking account or would rather invest it in the stock market. As a whole, Apple and other higher yielding saving opportunities would see lower inflows from consumer in a lower rate environment (the pie gets smaller). However, you’d assume that Apple would still capture a larger share of those inflows if they’re paying the most competitive rate.

I mean, even 2% is a good deal over 0.01%. Considering how easy it would continue to be for folks to create accounts, there’s going to be a pull as long as the majority of the market still things 1% interest is a thing their customers find attractive

")

Register on MacRumors! This sidebar will go away, and you'll see fewer ads.