Money today > money tomorrow. You can thank inflation for that. If you're already living on your own, then you're just throwing extra money down the drain by renting, as a mortgage (and everything that goes with it) it almost always cheaper then renting. With renting, you're paying the mortgage, taxes et al already, plus some profit for the landlord for going to the trouble to rent in the first place, and unlike buying, you don't have anything to show for the extra money you're spending at the end of the day/month.

Got a tip for us?

Let us know

Become a MacRumors Supporter for $50/year with no ads, ability to filter front page stories, and private forums.

Is it woth owning a house/property if you are going to be a single?

- Thread starter YS2003

- Start date

- Sort by reaction score

You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

you're only as far from civilization as your computer. and no matter where you go in this country, there's always a walmart within 1/2 hour. ups delivers anyplace there's an address in the u.s.

ok, i have to drive 1/2 hour to raleigh and then another 30 minutes to get to some cultural events there within the city limits. not really so bad. i got a couple chickens in my backyard and a goat. and a cat.

I am seriously not tryin to be ugly, but if you base your quality of life as being within 1/2 an hour of a Walmart....oh lawd! I got nothing to say.

On a more serious note. Home ownership will allow you to write off your property taxes. Depending on your income, you are either going to pay federal income tax or state property tax. Go for the house. Or a townhome if you dont want the yard upkeep.

I bought my first home when I was 22 for under 40K. I just sold it for 175K last year. I lived in it only 3 years and the rest of the time it was a rental house. Excellent tax write off, excellent income production, all round good investment.

as a mortgage (and everything that goes with it) it almost always cheaper then renting.

This doesnt hold true for even half the country. If you live in a rural or small city, yes it is true. But try to own in a larger city, the North East, California, Washington, etc and you cant touch the price of buying v renting.

I would recommend buying a condo. You generally won't have to worry about any external maintenance so it's less work overall (good if you're single - More time to have fun), but you can still build equity over time.

Actually, I think what you're saying is true, but only in and immediately around most large metro areas. I'm not sure that's anywhere near to being 1/2 the country though.This doesnt hold true for even half the country. If you live in a rural or small city, yes it is true. But try to own in a larger city, the North East, California, Washington, etc and you cant touch the price of buying v renting.

I am seriously not tryin to be ugly, but if you base your quality of life as being within 1/2 an hour of a Walmart....oh lawd! I got nothing to say.

Haha.. I think it was more a statement of proximity to civilisation, than a direct quality of life indicator.

Depends if you are speaking of population or area. Population wise, most people live within the major metropolitan areas that make ownership much more difficult.Actually, I think what you're saying is true, but only in and immediately around most large metro areas. I'm not sure that's anywhere near to being 1/2 the country though.

I wasnt trying to be argumentative. I have lived in California, Texas, Oklahoma, Florida, New York, and Illinois. Home ownership is different in each area. Here in Tx, the property taxes are as high as some places in the NE, I pay $16K a year. The gentleman I quoted lived in Alabama. Quite a different story.

Money today > money tomorrow. You can thank inflation for that.

actually you can thank the time value of money ...

a reverse mortgage is a horrible move and desperation type thing

Hang on a second. Do you (Americans) get to write your interest repayments off your tax? We can do that for a property you rent out, but not for your primary residence. Wow, I'd be able to eat every day if we could do that.

...owning a house/property is a must to build your net worth.

If you want to increase your net worth via real estate, i.e., buying at one price, selling at a higher price in the future...

Remember that house prices can go down as well as up.

Bricks and mortar are not a guaranteed 'investment'.

Remember that house prices can go down as well as up.

Bricks and mortar are not a guaranteed 'investment'.

Obviously, you want to be careful about where and what you buy. However, on average I have yet to see the value of a house go down and stay down as long as the owner keeps it up and works to keep the neighborhood nice. If he stays in the house for 30 years, there's a possibility that it may not go up as much as he'd hoped, but inflation and other factors will still make it worth more then than it was when he bought it.

One thing to consider is that the equity in a house can also be used towards retirement (perhaps this was mentioned in one of the later posts that I didn't read). Therefore, even if you don't have anyone to give the property to upon your death (although, who says a property has to go to family upon death?), it still makes sense to own it because the equity may come in handy for things like long-term care or other costs that arise after you retire.

Obviously, you want to be careful about where and what you buy. However, on average I have yet to see the value of a house go down and stay down as long as the owner keeps it up and works to keep the neighborhood nice. If he stays in the house for 30 years, there's a possibility that it may not go up as much as he'd hoped, but inflation and other factors will still make it worth more then than it was when he bought it.

That's all well and good, but what about unemployment/ill-health, negative-equity, recessions, bankruptcy and soon?

Remember that people were adamant that the Titanic was unsinkable.

A house, like the stock market, doesn't a guarantee a future return on your investment.

Depends if you are speaking of population or area. Population wise, most people live within the major metropolitan areas that make ownership much more difficult.

I wasnt trying to be argumentative. I have lived in California, Texas, Oklahoma, Florida, New York, and Illinois. Home ownership is different in each area. Here in Tx, the property taxes are as high as some places in the NE, I pay $16K a year. The gentleman I quoted lived in Alabama. Quite a different story.

Point taken. Property taxes here are among the lowest in the country, but we also have one of the highest sales taxes to "compensate" (9% here). But it still stands to reason that on a [newer/not yet paid off] home, buying is cheaper. The landlord has to make a profit over and above what he's paying on the house; I doubt there are many out there who just rent out a house at cost or less out of the goodness of their hearts.

actually you can take the time value of money ...

a reverse mortgage is a horrible move and desperation type thing

I agree. But if you're in a horribly desperate financial situation, you might be glad to do it

Well, right, ... nothing in life is guaranteed, other than death, right?That's all well and good, but what about unemployment/ill-health, negative-equity, recessions, bankruptcy and soon?

Remember that people were adamant that the Titanic was unsinkable.

A house, like the stock market, doesn't a guarantee a future return on your investment.

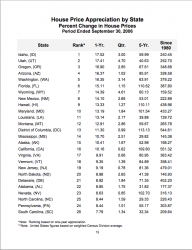

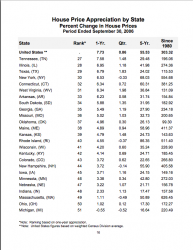

FWIW, attached are two pages from the Office of Federal Housing Enterprise Oversight (who knew we had one of them) showing the House Price Index.

Since 1980, the state with the least appreciation is Oklahoma, where houses only appreciated 99%. Looking at the other states, I'd guess that the average appreciation (since '80) is around 300%. I'm pretty sure that time period factors in some recessions, etc.

But like you said, nothing's guaranteed. A major terrorist attack around here would probably send the entire economy into the toilet (including property values), but in a situation like that, it's not like if you had your money invested anywhere else that it'd do much better.

Attachments

Well, right, ... nothing in life is guaranteed, other than death, right?

FWIW, attached are two pages from the Office of Federal Housing Enterprise Oversight (who knew we had one of them) showing the House Price Index.

Ahh, but are these figures adjusted for inflation? Because doubling or even tripling an investment in 27 years is not that much of an accomplishment, and might even be a regression in real terms.

Using an online inflation calculator, we get:

What cost $100 in 1980 would cost $253.97 in 2005.

So, something would have to be worth around 2.5X it's 1980 value, in 2005, to be breaking even in real terms. Sorry, the calculator wouldn't give me values for 2006, which would have better matched your figures.

Basically, what I'm getting at is that in many cases home ownership is worthwhile, but when there's a large enough difference between the cost to rent and own, then you might as well rent, and save and invest the difference.

If you're happy in your life (job, family, friends, location, etc) then, if you can, I would say buy a house. Definitely.

If you're not happy then what's wrong with renting? After all, this allows you to 'move around' until you a place/time where/when you want settle down to and make a home.

If you're not happy then what's wrong with renting? After all, this allows you to 'move around' until you a place/time where/when you want settle down to and make a home.

Buy the house...

If you decide you want to live somewhere else, rent it out and move somewhere else. Let them pay for your Mortgage.

I don't see much downside to being a home owner. It's more work (ie. lawn upkeep, repairs, etc), but your building up equity over the long run. That $1500/month is essentially going back to you in the long run.

If you decide you want to live somewhere else, rent it out and move somewhere else. Let them pay for your Mortgage.

I don't see much downside to being a home owner. It's more work (ie. lawn upkeep, repairs, etc), but your building up equity over the long run. That $1500/month is essentially going back to you in the long run.

Hang on a second. Do you (Americans) get to write your interest repayments off your tax?

The interest one pays on one's mortgage becomes a write off on taxes.

Well, right, ... nothing in life is guaranteed, other than death, right?

Don't forget the taxes....

Buying property is obviously something not to be taken likely. If you plan on settling in for a while and have done your research about the various areas to know which ones are good in terms of safety, development, infrastructure, etc, then buying is not a bad option for a single person. It all depends on lifestyle, priorities, and means. If you were to buy, I certainly wouldn't recommend buying something that is at the highest end of your affordability range--you want to be able to have a little room to grow and cover unexpected expenses. If the worst case scenario happens (heaven forbid) then at least the loss isn't as great as it could have been.

Ahh, but are these figures adjusted for inflation? Because doubling or even tripling an investment in 27 years is not that much of an accomplishment, and might even be a regression in real terms.

Using an online inflation calculator, we get:

What cost $100 in 1980 would cost $253.97 in 2005.

So, something would have to be worth around 2.5X it's 1980 value, in 2005, to be breaking even in real terms. Sorry, the calculator wouldn't give me values for 2006, which would have better matched your figures.

Basically, what I'm getting at is that in many cases home ownership is worthwhile, but when there's a large enough difference between the cost to rent and own, then you might as well rent, and save and invest the difference.

My home is worth 2x it's value in 4 years when I sold it. Better return than inflation.

Bottom line is, above even saving, home ownership should be the nnumber one prioirty (other than no credit card debt) over all other savings for any American. (not sure overseas) based on historical rate of return, tax benefits (interest payments are deductable) and general savings/investment habits of the typical American.

The individual saving rate in Japan is 30% per year. In the US it's -.5%. The average American loses money each year. A home with a decent mortage ( not a 1 year ARM) gives an individaual the ability to build equity that they can pull out at a later date via sale or refinance.

If you see a property you like, especially if you are going to be in an area for 2 or more years ( there's a 2-5 captial gains rule I'm not gonna get into here) buy as soon as possible.

Hang on a second. Do you (Americans) get to write your interest repayments off your tax? We can do that for a property you rent out, but not for your primary residence. Wow, I'd be able to eat every day if we could do that.

Yes we can. Maybe that's why we're all overweight

Register on MacRumors! This sidebar will go away, and you'll see fewer ads.