Because of "monetary" inflation.

There is no such thing as monetary inflation. There is only inflation or depreciation.

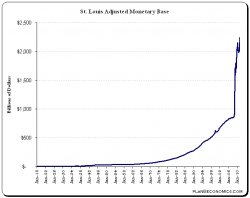

The increase in the M0, as indicated by the graph, shows a dramatic growth during the period from January, 2007 to January, 2010, much of it due to Fed actions aimed at stimulating the economy. Nonetheless, inflation (CPI-U) during that same period averaged 2.35% per year, hardly any cause for concern. At one time, particularly during the years between the world wars, the monetarist school of economic posited a direct relationship between the money supply and prices. Empirical evidence has shown, however, that increasing the M0 has little effect on prices, or inflation. Technically, the fallacy is a failure to fully understand what affects velocity, but in practical terms it means that consumers holding on to their cash, depositing it in banks and other M0 components, are reducing spending. Inflation is a function of supply and demand, and when an economy is in recession, there is little demand. Increasing the M0 will not persuade a consumer whose house and investments have lost value, who is newly adverse to incurring debt, and who is worried sick about losing his job to go on a spending spree.

The markets certainly agree that inflation is not an issue. Surely were inflation in the offing at a rate anywhere close to the rate of growth of the M0, no one would buy a five-year treasury bond with less than a 1% yield or a ten-year treasury with a 2.22% yield. The specter of inflation due to monetary policy is a bogeyman, and like all bogeymen it scares only the ignorant.

If Tim Cook or anyone else is worried about "monetary inflation" they should take out all the loans anyone will give them at current fixed interest rates. They could then easily pay back the loans with the inflated dollars they will be earning in the future. The fact that few want to take out loans--or to buy things, or to invest in property, plant and equipment, or to hire new employees--is the reason inflation will remain low until something other than monetary policy stimulates the economy. Dropping interest rates close to zero and providing easy money has done little to spur the economy, and an un-spurred economy will never produce inflation.

Now, depreciation--the decline of the value of the dollar relative to other world currencies--is a function of the relative performance of the economy of each nation. (Actually, the dollar's role as a reserve currency insulates it to some degree even from this principle.) Since we are in a global recession, the economies which support the euro are faring no better than that of the U.S. Consequently, the exchange rate between the dollar and euro was not very different in January 2010 from what it was in January 2007. Even where the underlying economy is strong, as in China, the Chinese Yuan Renminbi is a fixed currency, tied to the dollar (albeit somewhat more loosely lately), so there is little relative depreciation despite a roaring Chinese economy struggling with inflationary pressures. For China it is very important to keep its exchange rate relative to its trading partners low, so as to keep its exported products cheap. Again, though, there is no correlation between M0 and exchange rate. The Swiss franc, the currency you choose to prove such a correlation, is issued by the world's 27th largest economy. But even Switzerland, once a redoubt of monetarism, now manages to the three-month LIBOR in accordance with the SNB's statement of monetary policy. They are not philosophically opposed to increasing their money supply. In fact, the SNB increased its monetary base over the same 2007 to 2010 period from 44 billion to 90 billion CHF, essentially doubling its M0. Yet the exchange rate between the two currencies was about the same at the beginning of 2010 as it was at the beginning of 2008--and remember that efforts to address the housing finance crisis and the resulting liquidity crisis did not begin until the fourth quarter of 2008. Switzerland does attract, because of its historically investor-friendly, no-awkward-questions-asked policies, a great deal of foreign investment which it holds in its bank vaults, and which contributes to its reputation of having a sound currency. It is certainly considered one of the currencies of refuge, but not because the Swiss constrain their monetary base.

Accordingly, I don't think Tim Cook needs to worry that because the St. Louis Monetary Base has risen there will be inflation or depreciation or that the buying power of one million shares of Apple stock will be diminished.