i think the hardest thing for me is not knowing where apple pay is accepted. there's no emblems or markings in stores...

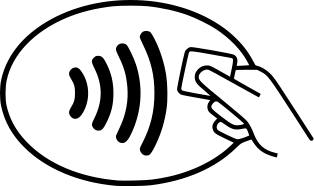

Either your location does things differently from where I am or you just don't know what to look for. Although I rarely see an ApplePay logo, I frequently see the contactless-card logo in stores:

Most places that display this logo work just fine with ApplePay. The only exceptions I've found are places (mostly MCX/CuttentC partners like CVS and Rite Aid) that have taken steps to deliberately disable ApplePay.

This is about the retailers waiting to get MCX up and running so they can cut out the middle man (credit cards) so they can mine data and also charge customers for payment transactions.

Bingo! Absolutely correct. Their goal is to hurt the credit card business, not improve the customer experience. See

this article from Business Insider, where (at the end of the article) former Wal-Mart CEO Lee Scott, when asked if he thinks CurrentC will work, is quoted as saying "I don’t know that it will, and I don’t care. As long as Visa suffers."

When you've got this kind of arrogance in charge of critical business decisions, you aren't going to get a decision that makes any sense.

It's so quick and easy to use chip & pin or contactless cards...

WRT chip-and-pin, yes. WRT contactless cards or chip-and-signature, no. If a contactless card is lost or stolen, it can be used fraudulently just like a swipe-based card.

ApplePay card numbers don't work apart from the phone/watch that they are assigned to, and if your phone is stolen, it requires fingerprint or PIN authorization in order to be used. This is much more secure than a contactless card (but is equivalent to chip-and-pin).

Yea, I don't see much benefit to using these smartphone payment systems just yet.

The benefit is the security. If you pay with ApplePay, and the merchant gets hacked, the hackers get a device-account-number that is useless when separated from your phone/watch. If you use a physical card, they get enough information to make fraudulent purchases and you have to deal with getting a replacement card.

Maybe, but banks in the US aren't issuing contactless cards either. They used to but used the same "low demand" excuse the retailers are using now to get rid of them.

Yes, it's the same excuse, but there's less justification.

A contactless card only adds a little security. Yes, there is (or should be) encryption going on so a system-hack won't let thieves produce a cloned card, but a stolen card can still be used until canceled. Ditto for any other kind of card, including chip-and-pin (although chip-and-pin cards will be much less usable after October, when merchants will end up liable for the fraud if the card is swiped.)

Apple Pay avoids all of this by using a device-specific account number that has no use whatsoever when separated from the phone/watch. And if your device is stolen, it will need to be authenticate by fingerprint or PIN, and can be remotely deactivated via the icloud.com web site.

In other words, there are clear security benefits to Apple Pay that are not really present with a contactless card. So I wouldn't expect customer demand for the two tow be identical.

... banks should make retailers partially liable for the cost of any fraud related to credit cards now...

Coming soon.

In October 2015 (for all but gas pumps, which will be affected in October 2017), all four major card issuers (MasterCard, Visa, American Express and Discover) are going to have new rules. See

this article describing the new rules.

Under the new rules, if your card has a chip, and the merchant doesn't process the card via that chip (that is, types in the number or lets you swipe it), then the merchant, not the bank, will be held liable if the charge turns out to be fraudulent. We should expect everybody's card to be replaced with chip-based cards, starting around when the new rules take effect in October, since the banks will want to shift the liability for fraud as soon as they can.

Once this happens, merchants are going to install and start using chip readers and NFC readers really fast, because they aren't going to want to be on the hook for fraudulent purchases made on their terminals.

So I went to Home Depot yesterday. They had NFC terminals, but they didn't accept my Apple Pay. When I asked the women working she said it was "hit or miss" if Apple Pay worked.

I think that's a matter of local store policy/setup. Where I am, it always worked at Home Depot.

HD is officially "coming soon" for Apple Pay, but as I understand it, individual store managers have been supporting it (via generic contactless payment card support) for over a year already.

Remember that Apple Pay is bad for retailers. With a standard credit card, they get your name and other information. ... But with Apple Pay, the retailer only gets a randomly assigned number for the transaction.

That's not true. They do get your name - I see it on the receipts from Apple Pay all the time. And while they don't get your card number, they get a device-account-number that acts as a stand-in for your card number. The DAN is specific to your phone, but it only changes if you remove and re-enroll your card.

WRT purchase tracking, using the DAN is a little less useful than a CC number, because multiple devices registered to the same card (your phone, your spouse's phone, your watches, etc.) will have different DANs, but they can still be used to track you.

Regional convenience store Sheetz (an MCX/CurrentC partner) will take my contactless master card at the pump, but the same card through Apple Pay is "unsupported".

Yes, and that's due to an explicit and deliberate decision to refuse to accept Apple Pay. That's not really the same thing as stores that just don't want to make the investment in NFC terminals.

I don't use Apple Pay even when it is available. I've found that it's faster or about the same amount of time to just swipe my AmEx card than to get Apple Pay to work.

You may feel differently if the merchant gets hacked and the hacker gets your AmEx card information, including all the security codes on the mag stripe. When this happens, they can make a new card with your info and place faudulent card-present transactions (which are often subject less scrutiny than card-not-present transactions, where only the card number is used.)

ApplePay (and chip-based transactions) are not nearly as easy to compromise via a vendor-hack, because there isn't a fixed set of security codes, but a dynamically-generated set produced via strong encryption.