it's a great concept and I like the physical card and potential cash rewards, but apple needs to seriously revisit the app:

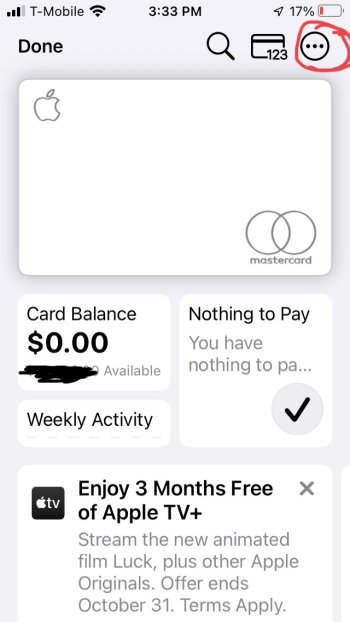

- 'Current Balance' is not actually the current balance. any purchases from the apple store using the card and the 'monthly installments' option are not reflected in the balance. instead, 'current balance' only shows the minimum payment due for that month. if you have already made that payment, the balance shows $0.00

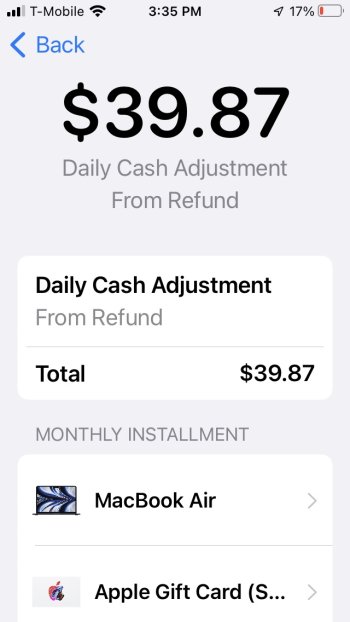

- the balance of the monthly installments items is buried in a sub menu

- the required minimum payment for an installment item shows up automatically as a new charge each month

- to pay off an item that is on monthly installments, you cannot just 'make a payment.' you have to go the installments sub menu and select 'pay early' even as your balance shows $0.00 since it does not reflect outstanding installments.

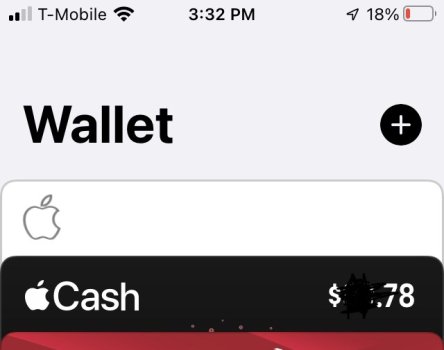

- cash rewards are reflected on a separate card in your wallet

- when a return is made, the corresponding cash reward shows as a new charge on the card. So if you earn a $5 cash reward on an item and then return that item...the $5 reward goes to the separate cash reward card in your wallet, and a new charge of $5 shows up on your card. It should just be a $5 reward on your Apple Card followed by a -$5 offset.

- in the app, the same charge will show under the 'previous statement' and 'most recent activity' making tracking activity difficult

All that to say...the card is advertised as easy to use and can help you track your spending, but you will need to create a spreadsheet with all the transactions, current monthly installment totals, cash rewards and cash rewards returns offsets just to figure out the actual real balance.